Schrodinger's Bubble

There are some pretty horrible “it’s a bubble” arguments out there about AI; lazy, poorly constructed and clearly written backwards (starting with the conclusion). I like to understand the opposing view and so, as an AI bull, I think it’s worth trying to steelman the bubble argument.

TLDR: even the best version of the argument depends on believing AI will not be sufficiently productive to pay for the datacentre investment. Ulitmately, I do not believe the argument to have any credence based on what we’ve already got diffusing and every new model increasing the TAM. However, I found the exercise constructive in terms of understanding the sceptics’ position and I think it will help me understand how they will react to news etc.

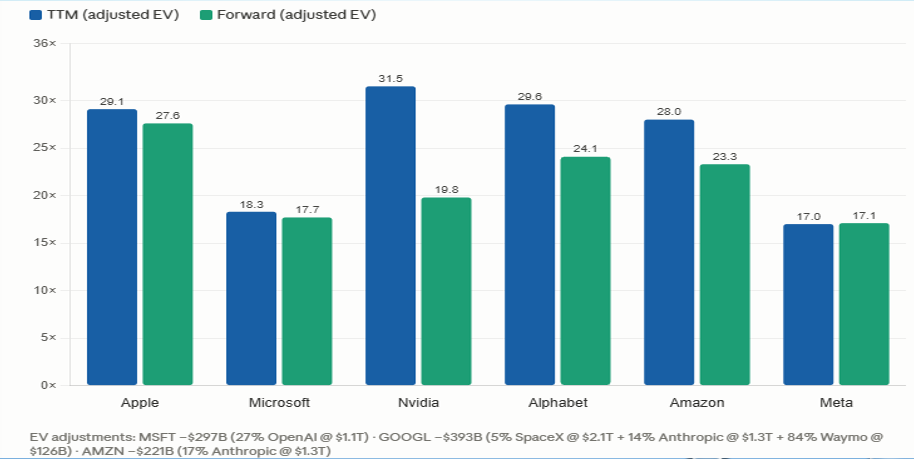

Let’s get the obvious out of the way. The first sign that a bubble is forming around a given narrative is if we can find evidence that there is a premium in stocks for merely being associated with the narrative in question. This is clearly not the case, at least not in the big stocks that matter (more on a potential small-cap bubble later). My evidence is a comparison of the Mag7 stocks excluding Tesla (its valuation had detached from reality long before AI):

It is well accepted that Apple is the least “AI pilled” of these stocks, and you can see that it is trading most expensive relative to forward earnings, the opposite of what you’d expect if arguing a bubble.

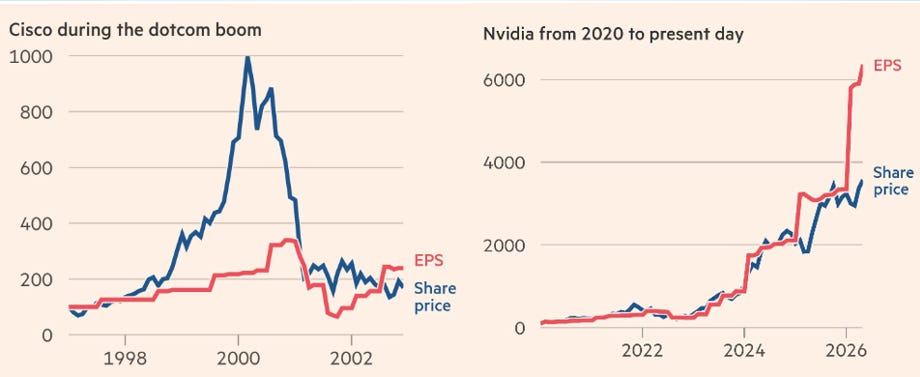

Next, one could look for evidence that share prices have diverged from their earnings. The FT of all places can help us out with that one, here’s a great graphic they came up with a few weeks ago:

Bye-bye, dotcom comparisons.

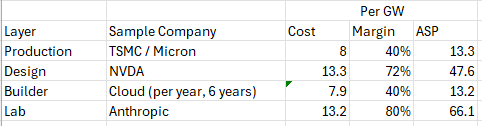

So the only argument left is that the earnings themselves are unsustainable. Here there is at least an argument worth making. There is a multi-layered industrial that goes into producing a frontier model and building the datacentre to serve it, and due to the current excess demand for use of these models, each layer of the stack is producing supernormal margins. A greatly simplified version of this might look like:

So, as consumers we are paying over $66B equivalent per GW per year for use of these models (this is for something like Opus High on an API rate; admittedly, other models and plans are much cheaper, but Fable is likely even higher). Also, the only reason the Production layer is so ‘cheap’ is because TSMC are so customer first they don’t like flexing their full pricing power. Micron meanwhile are charging closer to 90%.

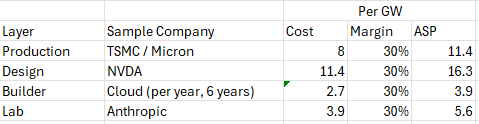

The multiplicative effect of high margins across multiple steps of the supply chain like this is enormous. To show this, all we need do is set the level to a more ‘normal’ rate across the whole chain:

I think it is this stark contrast that is at the heart of the bearish sentiment, even if the bears don’t express it well. We can then split their concerns into 2:

There’s no way AI can possibly be so useful as to justify itself at these price levels, so companies are either experimenting or leaning off susbsidised rates, there’s no way people will knowingly pay full price at scale for this stuff. This might have been a fine argument apriori, but it is a weak one now. This sounds like paying a software engineer per line of code: it’s just not how value gets created. AI will succeed or fail to be productive based on the quality of the output, and the cost will be relative to the cost of employing a human, not the hypothetical cost of building a datacentre cheaper.

The second one is about margin compression, and it is a scary thought for anyone long AI stocks, no matter how much you believe in the tech. Even if a GW year of datacentre capacity is producing a trillion dollars of value-add for end-users (which I can well believe btw), over time competition will push more and more of that value towards consumer surplus, and out of the profit margins of the companies involved.

I have no doubt that this is true, the only question is time, and this question is at the core of whether stocks are over or undervalued. Here I think we need to separate out Labs from the rest of the supply chain. For them, it is a question of whether their product is sufficiently better than the competition (especially open source) to justify a premium for usage. This is a never-ending race and I think there are good arguments for both sides.

For the rest of the supply chain, the question is how long the acute capacity shortage will last. We can map out reasonably well how quickly supply can scale up by looking at the various bottlenecks, including foundry capacity (rougly speaking >50% in 2027, then drifting down towards 30% over the coming years). What’s less predictable is demand, and in particular demand at prices that sustain this high profit ecosystem.

If you believe that demand growth will exceed supply for the next several years (or even decades) as I do, then this is a great time to own these big, high margin stocks. If you think that there will be significant spare capacity at datacentres at any time in the next 3 years, then you can reasonably call this a bubble. So I think there simulataneously is and isn’t a bubble, depending on your opinion of the usefulness of AI.

For those of us who believe that we are only scratching the surface of what can be achieved with existing models, and are optimistic about the frontier progress, this is a great time to own stocks. If we are right the truth will reveal itself slowly over time, and the market will adjust to that truth in the same period, punctuated by sentiment shifts between optimistic and pessimistic assessments of the set of facts at a given time. (For everyone else, there’s Mastercard!)

p.s. I do think there’s an interesting thing going on in small-cap stocks associated with AI. Here I genuinely do see bubble-like behaviour and valuations. My best guess at what’s going on here I’m going to call LADMO: Leopold Aschenbrenner Driven (fear of) Missing Out. There is a certain chunk of money seems to have collectively decided not only to go all in on AI, but to do it in small cap names where stocks can move 100% in a month. The total amount of money acting in this way probably totals $100-250 billion. Not enough to put a serious dent in megacap valuations, but enough to completely dominate small caps.